Table of Contents

Table of Contents

- What is an insurance bond for landscaping businesses?

- What are the benefits of having a landscaping bond?

- What does a landscaping bond cover?

- How does a landscaping bond work?

- What types of insurance bonds exist for landscapers?

- 1. Permit bonds

- 2. Performance bonds

- 3. Payment bonds

- 4. Business service bonds

- How do landscaping bond requirements vary by state?

- How much does a landscaping insurance bond cost?

- Factors that affect the cost of a landscaping bond

- How long does a landscaping bond last?

- How do you get bonded as a landscaping business?

- How do you renew or cancel a landscaping bond?

- What happens if a claim is made against your landscaping bond?

- What risks do landscaping bonds not cover?

- Where can you buy a landscaping insurance bond?

- How does an insurance bond differ from general liability insurance?

- How can Aspire help once your bond is in place?

Landscaping companies face a range of regulatory requirements to operate legally. They typically need a business license (or several) from the state and local governments where they operate.

In many cities, certain landscaping services, such as pesticide application, also come with their own regulations.

One common requirement for all landscaping businesses is securing an insurance bond.

This bond is often confused with an insurance policy, but the two aren’t the same, and many cities require both.

This article clears up any confusion you may have about the two concepts. It will cover:

What an insurance bond is

Why your landscaping business needs one

What bonding covers and the types available

State-specific insurance bond requirements

Cost and factors that impact it

How to get bonded

What is an insurance bond for landscaping businesses?

An insurance bond, also known as a landscaping license bond or surety bond, is a financial guarantee that assures clients that landscaping projects will be completed in accordance with state and local government-mandated guidelines.

It protects clients financially if your landscaping business doesn’t meet its obligations.

A surety bond isn’t the same as a regular insurance policy, which protects you from potential losses. Instead, it protects clients from your potential shortcomings.

Although, to be fair, there are benefits to an insurance bond for your lawn care business, as well.

What are the benefits of having a landscaping bond?

A landscaping bond helps you secure permits from the state and local governments, allowing you to legally operate a landscaping business.

It gives clients the assurance that you’ll complete their project in compliance with regulatory requirements.

Having a landscaping bond also:

Improves your company’s credibility: Being bonded demonstrates to prospects that you have their best interests in mind, are trustworthy, and financially capable.

Helps you meet contract requirements: Commercial and government clients require landscaping businesses to be bonded before hiring them for a project.

Provides competitive advantage: When competition for a project is fierce, bonds help you stand out. Potential clients will see the business as trustworthy, thus increasing your chances of being hired.

Covers theft and fraud liability: If your crew member steals from a client or defrauds them, being bonded protects you from embarrassment. Clients can claim the bond and be compensated.

What does a landscaping bond cover?

A landscaping bond protects clients if a lawn care business fails to meet the terms of the contract, doesn’t comply with regulations, or if one of its employees damages client property.

Here’s what the bond usually covers:

Incomplete and substandard work: The landscaping business couldn’t finish the project, or the quality was below the agreed standards. The bond will cover the client’s loss.

Breach of contract: The landscaping company abandoned the project and failed to fulfill its promises. The client can file a claim on the bond to be financially compensated.

Fraud or dishonest acts: For example, if the agreement was to use native plants suited to the climate because they’re low maintenance, but the landscaping company used invasive plants that spread aggressively, the bond can cover the client’s losses.

Theft from the client: If a landscaping employee steals items from the customer during a job, the bond is used to reimburse them.

How does a landscaping bond work?

An insurance bond serves as a passkey for governments to issue permits to your landscaping business and provides financial coverage for clients.

It involves three parties:

Principal: The landscaping business that buys the bond.

Obligee: The client that requires a financial guarantee and the government that needs the bond to license the business. The bond protects them if the business fails.

Surety: The company issuing the bond. It guarantees payments to obligees if there’s a valid claim.

The way it works is that the landscaping company (the principal) buys the bond. The cost is usually a percentage of the bond amount, set by the government or by client requirements.

If the company completes the project as defined by the agreement and regulations, nothing happens.

However, if it fails to deliver or operate as agreed, the client or government files a claim with the surety.

Next, the bonding company investigates the claim. If they find it’s valid, they pay the client up to the bond’s limit. The landscaping company has to reimburse the surety.

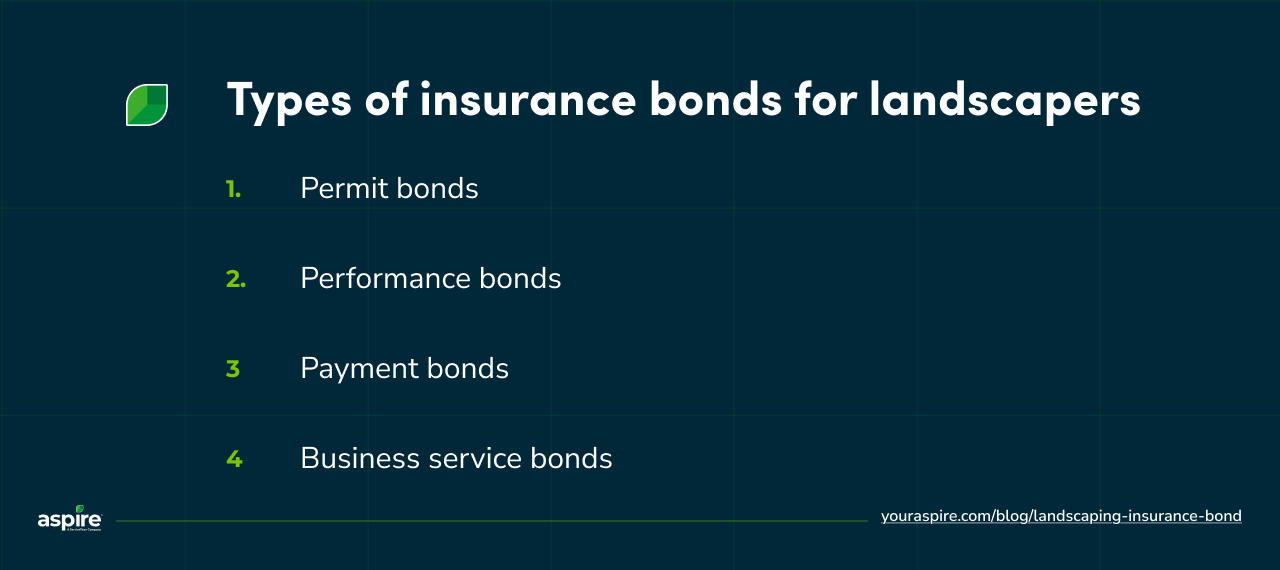

What types of insurance bonds exist for landscapers?

Even though bonds protect clients, there are several different types depending on the landscaping services you offer.

Here are some of them:

1. Permit bonds

Also called license bonds, these are typically required by state or local governments for your landscaping business to operate. A permit bond guarantees that your business complies with regulations.

It might also be needed to obtain specific business licenses from the city. In addition, clients request proof of permit bonds to confirm that your lawn care business is legitimate and compliant with government regulations.

You may need a permit bond if it’s required by the state or municipality in which your business operates.

2. Performance bonds

This bond’s purpose is to protect clients if a project isn’t completed in accordance with the terms of the agreement. Performance bonds are required by clients who need assurance that their funds are safe if the landscaping company defaults.

It ensures that the landscaping business either completes the job or compensates clients for non-performance.

3. Payment bonds

Landscaping businesses sometimes work with subcontractors, laborers, and suppliers on large projects. Payment bonds ensure that they get paid even if the landscaping company runs into financial difficulties.

Say a supplier has dropped off the last batch of pesticides, but the client hasn’t completed the project’s payment. The supplier can make a claim against the bond to recover their payment.

Once the client’s payment is received, the landscaping business reimburses the surety company.

4. Business service bonds

Employees who damage or steal the client’s property can cost your business dearly.

The client could end an ongoing contract or share negative reviews about your landscaping company, leading to a bad reputation. It can even damage the business.

A service bond saves you from such embarrassment by paying for damages. Clients get compensated, and your business remains safe.

How do landscaping bond requirements vary by state?

Insurance bonds’ requirements vary by state—some require bonds to issue landscaping licenses, while others don’t even have statewide permits.

Bond amounts also differ for states that require them. California, for instance, requires landscaping contractors to obtain a $25,000 license bond.

Oregon’s requirement ranges from $3,000 to $20,000, while North Carolina’s bond amount is $10,000.

Additionally, bond requirements vary within the same state, especially in states without a statewide bond requirement.

Local governments can impose additional bonding rules for landscaping businesses.

For example, the state of Illinois doesn’t require landscaping bonds, but specific regions, such as the Village of River Forest, Rolling Meadows, or the City of Markham, do.

Because of these differences, you need to check with the state and local licensing board to confirm what’s expected of you.

How much does a landscaping insurance bond cost?

A landscaping bond costs between one and 15% of the coverage amount, with the pricing dependent on what you need. For example, if your bond is $50,000, you can expect to pay a premium between $750 and $7,500 per year.

The actual cost depends on factors such as your credit score (a good credit score means a lower premium and vice versa), bond amount, business history with the surety company, and the bond term.

Factors that affect the cost of a landscaping bond

Here’s a breakdown of the different factors impacting bond cost:

Bond amount: Getting a high bond limit, e.g., $100k or more, means you’ll probably pay a higher premium.

Credit score: A low credit score means you’re a high-risk applicant, and surety companies will demand higher premiums. Applicants with good credit scores are likely to get lower premiums because they’re considered low risk.

State requirement: Bond amounts vary by state and municipality.

Business experience: Surety companies trust landscaping businesses with years of operation and a good reputation. It means they have a low risk level and may be eligible for more affordable premiums.

Bond length: The duration of the bond can affect the cost. Shorter periods tend to attract lower costs, while longer terms attract higher premiums.

How long does a landscaping bond last?

A landscaping bond ideally lasts one year; however, the exact term depends on the type and purpose.

Bonds that help landscaping companies secure licenses might need to be renewed annually since they’re tied to your business permit period.

A bond might also be dependent on a landscaping project, lasting only for the duration of the job. A good example is the performance bond.

Bonding companies’ policies may also affect the bond’s duration.

How do you get bonded as a landscaping business?

You can apply for a landscaping bond using the steps outlined below:

Check state and local requirements: Visit government websites or physical offices where your business operates to learn what’s expected of you. Confirm the permit bond amount your business needs.

Identify the bonds you need: Besides permit bonds, there are other bond types you might need to protect clients and your business reputation. Evaluate your target audience and current project to define the appropriate bond. For example, if you’re trying to bid on commercial or government projects, getting a performance or contractor bond might help you stand out.

Find and apply to a surety company: Search for bond providers in your state and contact them for an overview of their policies. Many insurance companies also offer bonds, so you can check with your insurance agency. Once you’ve found a surety company, you can apply by providing the necessary business information. They will usually ask for:

Business name, location, and license details

Owner’s personal and business credit history

Financial statements (for higher-value bonds)

Project or service details for performance bonds

Required bond amount

Get your bond certificate: Surety companies will use the information provided to calculate your premiums and give you an offer. If you like the deal, pay the premium and sign the necessary paperwork to activate your bond. You can submit the proof of bond to the licensing authority and keep a copy for your records to show clients who need assurance. Lastly, confirm the bond’s duration with the government or bonding company.

How do you renew or cancel a landscaping bond?

When it’s time to renew your bond, surety companies sometimes send out notices 30 to 90 days before the renewal date. It typically comes as an invoice link or a form you need to complete.

Even if you don’t receive a reminder, it’s still your responsibility to renew your bond in time. Here’s how to do that:

Contact the surety bond: Let them know you’d like to renew the bond. You shouldn’t have to provide additional documents or sign any paperwork unless you’re making changes to the bond.

Submit renewal forms and make payment: Send the new forms to the surety company along with the renewal payment. Ensure this is done before the renewal date.

Receive the bond certificate: After payment is confirmed, you should receive the certificate via email or in your P.O. Box within a couple of days. Confirm the information on the bond is correct.

What happens if a claim is made against your landscaping bond?

If a claim is made against the landscaping bond, the surety company expects that you respond to the issue. Failure to do this means they’ll contact you and the claimant and start an investigation as to the claim’s validity.

If the investigation finds the claim to be invalid, no action will be taken. However, you may be liable for any cost incurred by the surety company.

But if the claim is valid, you can choose to resolve the issue by:

Compensating the client

Presenting a valid defense to the claim

If the surety company financially compensates the client, you will be required to reimburse it for the amount paid and any related costs.

What risks do landscaping bonds not cover?

Landscaping bonds guarantee clients the completion of a project and provide compensation if project agreements aren’t met.

They don’t cover:

Losses: If an employee is injured at work, bonds do not provide protection. Only workers’ compensation insurance does that. Similarly, equipment insurance, not bonds, protects you if your landscaping equipment is stolen or damaged.

General business liability: In the case of damage to a client’s property caused by equipment, subcontractors, or poor workmanship, bonds don’t cover it. That’s where general business insurance comes in handy.

Vehicle challenges: Your vehicle was in an accident or damaged? You’ll need vehicle insurance, not a bond, to handle the situation.

Natural disasters or events: A weather delay has caused you to shift the project’s completion date by a week, or a heavy storm destroyed the native plants you just planted. You need business interruption insurance to cover the lost income and ongoing expenses.

Where can you buy a landscaping insurance bond?

You can get an insurance bond from any of the options below:

Bond agency/brokers: They’re professionals who can help you find the right bonds for your lawn care business. The Small Business Administration has a database of agencies you can choose from.

Online bond providers: These are websites where you can get quotes, compare pricing, and purchase bonds online in a matter of minutes. Some examples include Surety Bonds or Zip Bonds.

Insurance companies: Many insurance providers have a surety bond department that can issue license, performance, or service bonds. The process can be done digitally, so it’s pretty seamless.

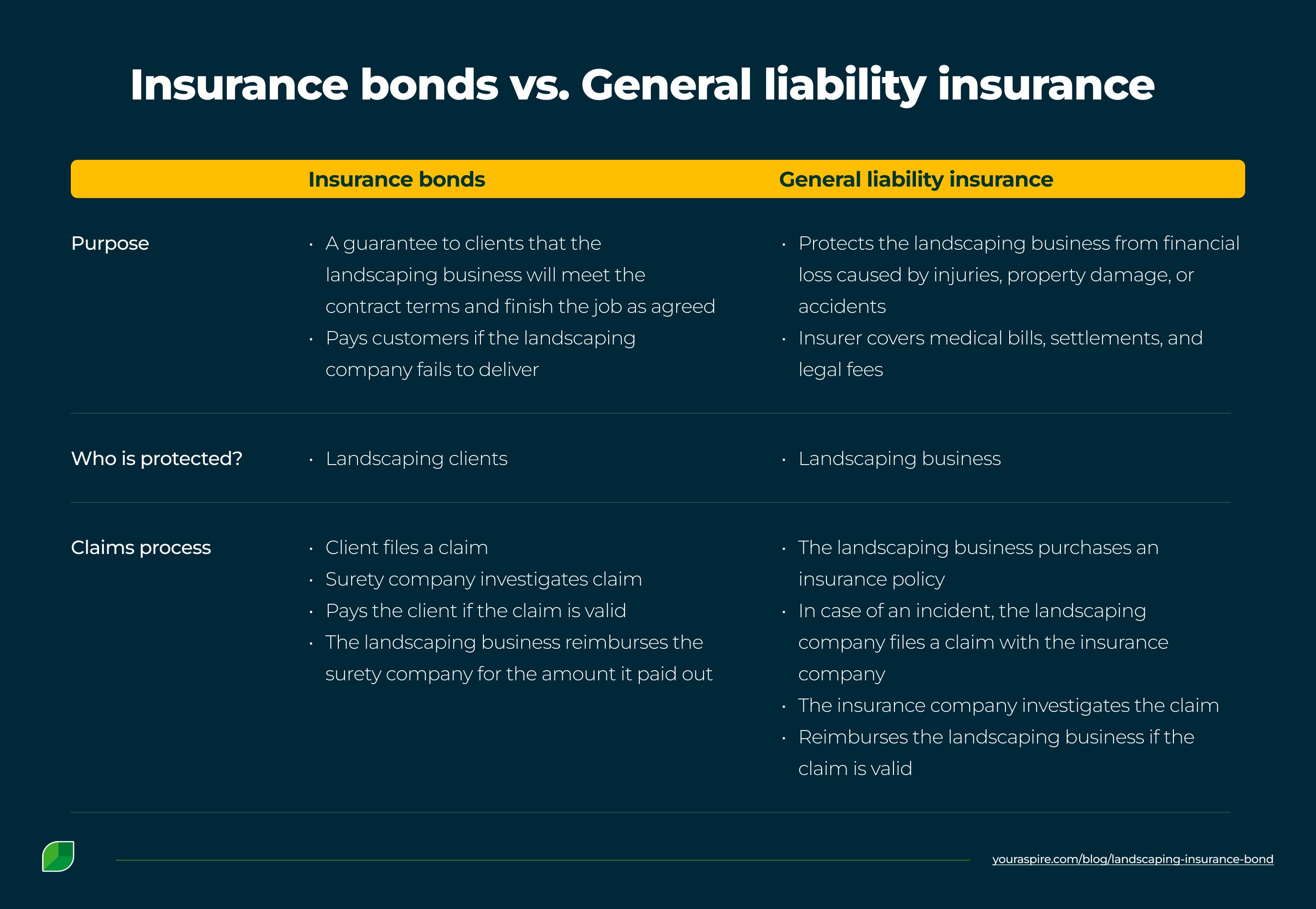

How does an insurance bond differ from general liability insurance?

Liability insurance protects your business from losses, injury, or damage—incidents that can upset operations. Unlike bonds, it’s not about the client; it's about safeguarding your company from theft, lawsuits, or claims arising from injuries, negligence, or unforeseen circumstances.

Bonds, on the other hand, protect landscaping clients from financial loss if a project isn’t completed as agreed, an employee steals from them, or there are fraudulent dealings.

Insurance bonds and liability insurance both protect your lawn care business, but in different ways. One (bonds) keeps you from a bad reputation, and the other from financial loss.

How can Aspire help once your bond is in place?

Getting an insurance bond is important for landscaping businesses. But you know what’s even better?

Never giving clients a reason to file a claim against it. That’s how you protect your reputation and bottom line.

Imagine running your landscaping company with almost zero complaints and clients raving about your work to everyone they know.

Aspire helps make this a reality by providing features that keep your business organized, efficient, and running smoothly.

Here’s an overview of some of these features:

Estimation: Use historical job data to create accurate estimates in just a few minutes. You never have to risk missing crucial details by manually creating bids again.

Incident reporting: Aspire simplifies how clients and crew members report incidents in the field, ensuring a swift response. Clients have a customer portal where they can lodge complaints, and crews have an incident screen on Aspire to add incidents as they happen.

Scheduling and job management: Once you’ve landed a new project, Aspire lets you add it to a schedule board that looks like a calendar.

From there, you can assign crews to jobs. This way, you have a clear overview of who’s responsible in case of client complaints.

Quality control tracking: Aspire enables the landscaping crew to provide real-time project progress from the field. They document the process by taking photos and writing notes, which can be uploaded to the client portal for customers to view. This creates transparency and proof for your records in case concerns arise.

Want to see other ways Aspire helps you take charge of the business to prevent complaints and avoid claims on your bond?

Book a free demo with Aspire today.