Table of Contents

Table of Contents

- What does it mean to be insured and bonded in lawn care?

- Why do lawn care businesses need insurance and bonds?

- What types of insurance are required for lawn care businesses?

- What types of bonds do landscaping businesses typically need?

- How do you get insured as a lawn care or landscaping business?

- How do you get bonded for lawn care work?

- How much does it cost to get licensed, insured, and bonded?

- How does being bonded and insured protect your clients?

- What happens if a lawn care business is not bonded or insured?

- Are there differences in insurance and bond requirements by state or city?

- How do bonds and insurance help grow a lawn care business?

- How do you renew your lawn care insurance and bond?

- How Aspire can help

Obtaining insurance and bonding for landscaping businesses is a licensing requirement in most municipalities and cities.

But beyond meeting permit requirements, getting insured provides your business with:

Legal protection from unforeseen incidents

Credibility in the eyes of prospects and clients

This, in turn, allows you to win contracts, operate freely, and avoid liability.

If you’re just starting, it’s crucial to understand what insurance and bonding involve. Without proper guidance, you risk paying for unnecessary coverage, being underinsured, or facing high future costs.

This article will cover all you need to know about insurance and bonding in the landscaping industry, including:

Why being insured and bonded matters

Types of insurance and bonding needed in landscaping

Steps to get insured and bonded

The cost involved

The risks of skipping insurance coverage

What does it mean to be insured and bonded in lawn care?

Being insured means that your lawn care business has coverage if an incident happens while you’re providing landscaping services.

For instance, if a crew member is injured on the job, landscaping insurance provides financial protection for medical costs and lost wages.

Being bonded means you’ve purchased a surety bond—a financial guarantee to clients—proving that you will either complete the project or compensate them if you’re unable to.

If anything happens with the project, e.g., if the contract is breached or theft occurs, the client can file a claim against the bond for financial compensation.

Both terms are often mentioned together because they build trust with:

The government (state or local) that assigns you a permit

Employees who work for you

Clients who pay you for lawn care services

Why do lawn care businesses need insurance and bonds?

Landscaping businesses need insurance policies and bonds to protect the firm, its clients, employees, and reputation while meeting legal and licensing requirements.

Here’s a breakdown of why they’re important:

Financial protection: It’s typically your responsibility when incidents such as employee injuries, client lawsuits, or equipment-related property damage occur. If you have insurance, it covers costs for damages, medical bills, repairs, and legal bills.

Risk management: As your landscaping business grows, insurance and bonding help manage risks so an incident doesn’t damage your reputation or impact operations.

Boosting client confidence: Clients feel more confident in your lawn care business when they know they’re protected if, for some reason, you can’t complete the job or damage occurs. Being bonded and insured gives them that peace of mind.

Meeting licensing requirements: Different cities and counties require proof of insurance or bonding to issue landscaping licenses. Without them, it might be difficult for you to operate legally or earn prospects' trust enough to win contracts.

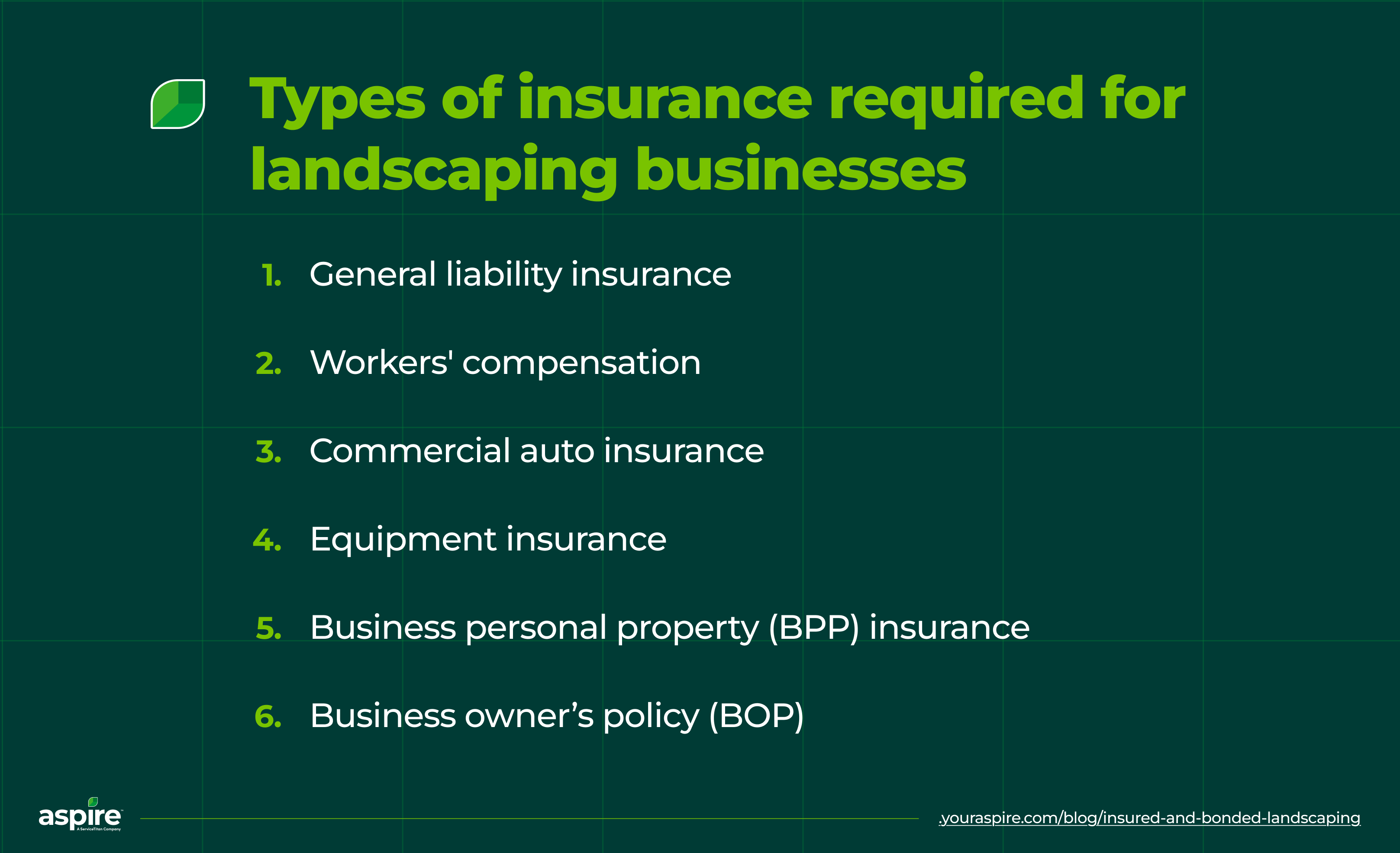

What types of insurance are required for lawn care businesses?

To ensure your business remains protected when incidents happen, here are the insurance types you’ll need…

1. General liability insurance

General liability insurance covers common risks like property damage, injuries (client and worker), defamation, or copyright infringement.

It will cover repairs, medical bills, and legal costs in case of an incident.

2. Workers’ compensation

Picture this: a member of your landscaping crew has just been injured by a mower blade or tree trimmer.

Because this happened in the field, it’s your responsibility as the employer to cover their medical bills and ensure they’re provided for until they can return to work.

Workers’ compensation covers the following:

Immediate medical costs like ambulance rides, emergency ward visits, surgery, etc.

Wages while the employee is unable to work.

Ongoing medical care, such as medication.

But this insurance type isn’t just for a landscaping crew; it’s for business owners, too. If a worker decides to sue over an injury or incident, workers’ compensation will help cover settlement, court costs, and other legal fees.

3. Commercial auto insurance

Commercial auto insurance will cover medical bills for anyone involved in a collision with a work vehicle, as well as legal expenses and property damage arising from the accident.

Instead of paying for all this out of your own pocket, the insurance pays for it, saving your business thousands of dollars.

4. Equipment insurance

Has some of your landscaping equipment been stolen, damaged, or lost?

An equipment insurance policy provides coverage for the repair or replacement of your damaged tools.

Equipment insurance typically covers transportable tools such as lawn mowers, leaf blowers, and wheelbarrows. Its coverage applies when the equipment is stored in a truck or at a job site, or is being transported to different locations.

5. Business personal property (BPP) insurance

BPP protects you against damage, loss, or theft of business property, including computers, furniture, heavy machinery, and office equipment.

Whether you own or rent your office space, BPP covers any property damage. If the landscaping company is run from your home, the coverage extends to the items used in the business.

6. Business owner’s policy (BOP)

This insurance type is a combination of general liability insurance and commercial property policy. It provides liability and property coverage for your business. Here’s a list of things included in the BOP:

Client injury

Damaged customer property

Damaged business property

Advertising injury

What types of bonds do landscaping businesses typically need?

Here are the different types of bonds you may require to run your landscaping business…

1. License and permit bonds

Permit bonds are required if you are to get landscaping-related licenses from the municipalities where your business will operate. They protect the government and customers by holding the landscaping business accountable to the corresponding federal, state, or local regulations.

If you don’t abide by the landscaping laws in your municipality, clients can make a claim against the bond. They get reimbursed, and you have to pay the surety back the same amount. You may even lose your license.

2. Performance bonds

Working on a high-value municipal job, commercial contract, or residential landscaping project?

Performance bonds guarantee clients that the landscaping project will be completed in accordance with the contract’s terms and standards.

If not, the customer can make a claim against the bond and get reimbursed.

This bond is especially important when working on government projects because of the Federal Miller Act and the Little Miller Acts. It’s a law that requires contractors handling projects over $150,000 to post a performance bond that protects the government and the client.

3. Payment bonds

This is similar to performance bonds, but instead of protecting the government or clients, payment bonds protect suppliers and subcontractors working with you on large projects.

It ensures they’re paid for the material and labor supplied. If you’re unable to pay them, they can file a claim to recover their money.

4. Fidelity bonds

Also known as service or janitorial bonds, this option protects your clients in the event that an employee steals or damages property while on their premises.

It also protects you from unethical employee behavior that could cost your business.

While it’s not always mandatory, some clients (especially commercial or large institutions) may ask for it before doing business with you.

How do you get insured as a lawn care or landscaping business?

To get your landscaping company insured, here’s a step-by-step guide on what to do:

Evaluate your risks: Assess the landscaping services you provide and identify potential risks involved. For instance, if you offer mowing, snow removal, tree trimming, or fertilization services, you may face risks such as employee injuries, equipment theft, or property damage. By knowing the risks involved, it becomes easier to identify the right insurance policies for the company.

Research insurance requirements: Check your city or state's requirements, as some may require proof of insurance before issuing a business permit. Look for what type of coverage is needed and the specified limit. This can guide the insurance policy you get.

Define the coverage you need: Based on your risk assessment and the policy requirements in your state or city, choose the insurance coverage that is right for the business. This could be general liability, commercial auto, workers’ compensation, or equipment insurance, as discussed earlier.

Compare insurance providers and choose a vendor: Request quotes from different vendors to compare rates, coverage limits, deductibles, and policies. Which one of them has more experience dealing with lawn care businesses? Those are the ones to really look into, as they better understand the risks you face. Do they also meet legal requirements? You can also use an insurance broker if you don’t have a lot of time on your hands. Once you’re satisfied with your research, select a policy that aligns with your needs.

Compile necessary information: Check what the insurance vendor you’ve selected requires from you. You may need to provide:

The number of employees on your payroll

Business license details

Annual revenue

List of equipment and vehicles

Landscaping services offered

6. Review and purchase: Before signing the insurance policy, carefully read the fine print. Involve your lawyers in the process so nothing takes you by surprise later on. Ensure you also keep digital and printed copies for your records.

7. Update your coverage regularly: As the business grows and you add more services, reassess your coverage annually. Check if there have been changes to your agreement with the insurance vendor.

Update your policies as you hire additional employees, acquire more equipment, add new services, or expand into new locations.

How do you get bonded for lawn care work?

Getting a bond for your landscaping business is pretty straightforward and can be done online. Here’s how you can do it:

Check local requirements: Municipalities sometimes require proof of bond to issue landscaping permits. Ensure you check with the local clerk’s office what type of bond is needed. You also want to examine your coverage requirements to choose an appropriate bond for the business.

Find a bonding company: Look for a licensed surety provider in your state, specifically, companies that have experience working with landscaping businesses. This could be an insurance company, which can often provide bonds as well.

Submit your business information: Most bonding companies will ask for details such as your:

Business name and license details

Owner’s personal and business credit history

Financial statements

Project details if you’re securing a performance bond

Annual revenue

Years of experience

Landscaping services provided

Business equipment, supplies, and property

4. Pay the premium and get your bond certificate: You’ll need to pay a small annual fee. Once payment is made, your business is bonded with a certificate or proof of bond.

How much does it cost to get licensed, insured, and bonded?

The cost of getting your landscaping business licensed, bonded, and insured varies by state and city. It could range from free to over $1,000, covering application fees, examination costs, and tax registration fees.

Here’s an overview of what it could cost:

Business license (including business registration, exam, and application fees): $30-$500.

General liability insurance: $50–$100 per month.

Commercial auto insurance: $200–$300 per month.

Workers’ compensation: $14–$45 per month.

Equipment insurance: $19–$80 per month.

Business property insurance: $50–$100 per month.

Business owner’s policy: $30–$80 per month.

Landscaping bond: Typically costs one to five percent of the total bond amount per year.

Several factors can influence insurance or bond costs. They include:

Bond amount: Higher coverage means higher monthly premiums.

Risk level: If your services are considered high-risk, your premiums may increase.

Business history: Does your business have a clean financial record? You may qualify for lower monthly premiums.

Number of employees: More crew members means you could pay a higher insurance fee.

Business size: A big landscaping company has more to insure and, as such, could face higher monthly payments.

How does being bonded and insured protect your clients?

Bonds compensate your clients when there’s a breach of contract or unethical behavior from your team.

By entering into a bond surety, you enter into an agreement with the bond company and the client. If you fail to meet the agreement, the client can be refunded by the surety firm for their financial loss.

For instance, say the client has prepaid for a patio reconstruction project, and you couldn’t finish the work or didn’t meet their expectations. The bond can be used to reimburse the client.

Insurance, on the other hand, covers the cost of property damage, accidents, injuries, loss, fire outbreaks, or theft.

A crew member accidentally breaks a client’s window when a trimmer picks up a rock? Your insurance can cover the repairs instead of the client (or yourself) paying the expense.

Both bonds and insurance give your clients peace of mind. It makes them feel safer knowing there’s a system for reimbursement if something goes wrong.

What happens if a lawn care business is not bonded or insured?

Landscaping businesses that aren’t insured or bonded risk huge financial losses as they become financially responsible for costs related to accidents, injuries, lawsuits, unpaid wages, or property damages.

Beyond the financial impact, failing to be bonded or insured can:

Damage your reputation: Clients might hesitate to do business with a company that doesn’t have any coverage.

Prevent the business from obtaining a license: Some cities require landscaping companies to provide proof of insurance and bonds before issuing a license.

Make you lose huge projects: Many commercial and government contracts require proof that you can complete a project after an up-front payment. Not having a bond or insurance puts your business at a disadvantage.

Get the business sued: If you start a landscaping business without the required permits and licenses, you risk being sued by clients and the government.

Are there differences in insurance and bond requirements by state or city?

Yes. The requirements for insurance policies and bonds differ by state and city.

While some states need proof of insurance before granting permits, others have no such requirements. New York, for example, requires workers’ compensation insurance, even if you have just one employee.

Because the rules vary greatly, it’s best to check with your local business or licensing offices.

They can provide up-to-date information on:

Bond amounts needed

Documentation processes and renewal deadlines

Specific insurance policies required

How do bonds and insurance help grow a lawn care business?

Being bonded and insured helps grow your landscaping business by:

Building trust with prospective clients: Customers feel more confident hiring a business with bonds and insurance. This assures them of a refund if their expectations aren’t met or an incident occurs. As a result, they will be more willing to sign a contract and even refer others.

Providing financial stability: Insurance helps cover emergencies and incidents. Bonds protect clients if a project isn’t completed as agreed. Both help you avoid financial setbacks that could stall business growth and expansion.

Attracting high-ticket clients: Customers like government agencies, commercial properties, or high-end residential buildings usually require proof of insurance or bonding before hiring a contractor. Having both puts you in a good position to secure contracts from them.

Strengthening your brand reputation: Being insured and bonded shows you’re concerned about your clients’ best interests. This can lead to positive reviews, referrals, and repeat clients.

How do you renew your lawn care insurance and bond?

Insurance policies and bonds aren’t one-off investments. You need to extend them frequently—insurance is renewed on a six-month or annual basis, and bonds are renewed yearly.

But it’s a straightforward process that might vary depending on your provider.

Here’s how it typically goes for insurance policies:

Check your policy expiration date. While insurance companies send reminders a couple of months before the expiration date, it’s best to add it to your calendar.

Review the business’s coverage needs. If the business has expanded or contracted, update the policy to ensure you’re properly insured.

Submit required documents. Some insurers may need proof of business growth and financial records for the renewal.

Pay the renewal fee and receive the certificate of insurance.

Here’s how to renew bonds:

Know the bond’s term (most last one year, so keep that in mind).

Contact the surety company about the renewal and submit any required information.

Pay the bond premium and file the renewed bond with licensing authorities.

How Aspire can help

Insurance and bonds are financial instruments that protect your business when you can’t meet contractual obligations or cover damage costs.

To acquire them, you typically have to provide information on business operations, sales, and services provided.

Aspire makes it easy to compile and share such information when dealing with insurers and bond issuers.

With tools for reporting, scheduling, estimation, and job costing, Aspire enables you to manage your landscaping operations more professionally from a centralized location.

As a result, it’s easier to gather the data insurers and bond issuers need.

See how this works in real time yourself. Book a demo with Aspire today.