Table of Contents

Table of Contents

- What is retirement planning for landscapers?

- Why is retirement planning important for landscapers?

- What are the biggest mistakes landscapers make in retirement planning?

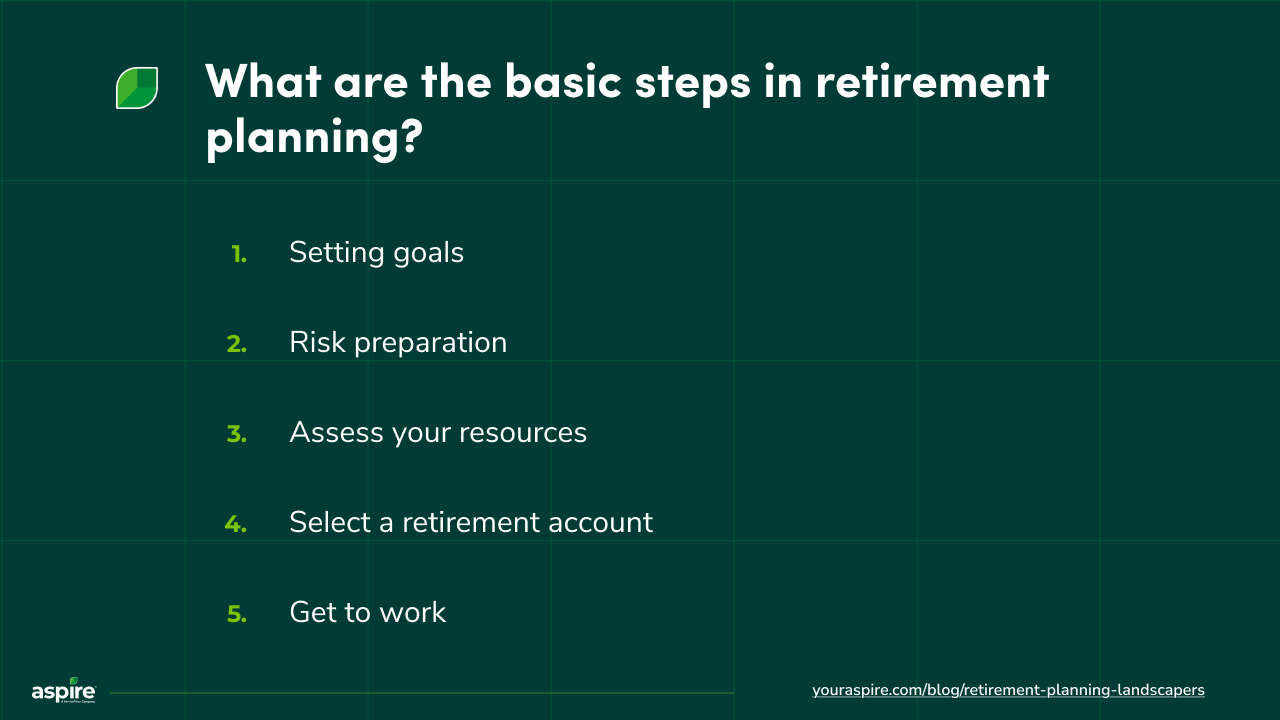

- What are the basic steps in retirement planning?

- 1. Setting goals

- 2. Risk preparation

- 3. Assess your resources

- 4. Select a retirement account

- 5. Get to work

- How much should landscapers save for retirement?

- What are the best retirement savings options for landscapers?

- When should landscapers start planning for retirement?

- Is it ever too late for landscapers to start saving for retirement?

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- Is it ever too late for landscapers to start saving for retirement?

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- When should landscapers start planning for retirement?

- Is it ever too late for landscapers to start saving for retirement?

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- What are the best retirement savings options for landscapers?

- When should landscapers start planning for retirement?

- Is it ever too late for landscapers to start saving for retirement?

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- How much should landscapers save for retirement?

- What are the best retirement savings options for landscapers?

- When should landscapers start planning for retirement?

- Is it ever too late for landscapers to start saving for retirement?

- How can landscapers sell their business to fund retirement?

- How can landscapers maximize retirement income?

- How Aspire helps landscaping business owners prepare for retirement

- What are the basic steps in retirement planning?

- What are the biggest mistakes landscapers make in retirement planning?

- What are the basic steps in retirement planning?

- Why is retirement planning important for landscapers?

- What are the biggest mistakes landscapers make in retirement planning?

- What are the basic steps in retirement planning?

- What is retirement planning for landscapers?

- Why is retirement planning important for landscapers?

- What are the biggest mistakes landscapers make in retirement planning?

- What are the basic steps in retirement planning?

Did you know that about six in 10 Americans have a retirement savings plan?

That sounds good, until you realize that one in five small business owners, including landscapers, have nothing saved for retirement.

And the ones that do? Saved less than $50,000.

This isn’t surprising when you consider the challenges: irregular income, limited time for financial planning, and uncertainty about long-term savings.

Still, planning for retirement is crucial. Not just for your peace of mind, but also to ensure you’re financially secure when you step away from the landscaping business.

This guide will walk you through how to start and maintain a retirement plan tailored to your business model and lifestyle.

TL;DR:

Saving early helps you retire comfortably, given how physically demanding landscaping can be.

Plan to contribute 15% of your gross income into a retirement savings account.

Diversify your investment to maximize retirement income.

Set up automatic savings to remain consistent with your retirement goals.

What is retirement planning for landscapers?

Retirement planning for landscapers is a detailed strategy that outlines how to save for retirement despite challenges such as limited profits or the need to reinvest in the business.

It begins with defining your financial goals and risk tolerance, and then implementing systems to ensure a comfortable retirement in the future.

Retirement planning for landscapers should involve steps like:

Saving consistently

Choosing the right retirement savings account

Investing your savings

Planning for taxes and health care

Restructuring your landscaping business to generate passive income later or to sell it

Why is retirement planning important for landscapers?

Planning for retirement gives you confidence that your future is secure. Considering landscaping is physically demanding work, it’s not something you want to do well into your 60s and beyond.

A retirement plan ensures you can comfortably step back when your body says it’s time without worrying about your finances.

Secondly, landscaping is seasonal. One minute, you’re all booked during summer, and the next, you’re hoping clients come knocking during the winter season. Income can be unstable.

Planning helps you build savings during strong months to support your retirement goals.

Thirdly, the absence of employee benefits is another reason to plan for retirement. Most landscapers are self-employed or work for small to midsize businesses that don’t offer retirement plans. Being proactive with retirement plans ensures your future finances are secured.

Lastly, retirement accounts like 401(k)s or SEP IRAs offer tax benefits that help reduce your taxable income. This enables you to save funds as you build for the future.

What are the biggest mistakes landscapers make in retirement planning?

Certain mistakes can disrupt your efforts to make a solid retirement plan, leaving you unprepared when it’s time to slow down or step away from active work.

They include:

Starting too late: Your profit margin is relatively low, you’re trying to build the business, and there are crucial bills to pay. These are all reasonable reasons why landscapers delay retirement savings. But the truth is, there’s never a good time. Delaying only makes it harder to accumulate the funds you need to reach your retirement goals. So if you’ve been putting off your start date, here’s your sign to start now.

Not having a comprehensive plan: Without a clear strategy, it’s difficult to estimate how much money you’ll need or a realistic timeline for retirement. A plan serves as a roadmap for saving, investing, and tracking your progress.

Underestimating key expenses: Failing to factor in real estate, health care, or inflation can quickly eat away at your savings. You need to make plans for current daily expenses to keep your retirement savings intact.

Mixing retirement savings with personal savings and business finances: It’s very easy to mistake retirement savings for personal savings, especially when there’s an emergency. But this can drain your future funds if you’re not careful. Try to keep each fund in a dedicated account to ensure it’s used as intended.

What are the basic steps in retirement planning?

Ready to plan for your retirement?

Here’s how to get started:

1. Setting goals

You need an idea of the following:

The age at which you want to retire and the lifestyle you’d like.

The amount of monthly income you will need to make this possible.

The additional ‘rainy day’ money you’ll need to cover emergencies, home repairs, and health expenses in your retirement.

The extent to which inflation between now and retirement will lessen the power of your savings. Your regular retirement contributions will have to compensate for this.

Next, figure out when you would like to start saving. What percentage of your income is enough to fund your goals?

Then, set up systems to help deduct savings.

2. Risk preparation

Mentally and strategically prepare for risks in advance, because there will always be uncertainties. The stock market could crash, the economy could tumble, and medical costs could shoot up.

You must be prepared to navigate challenges, especially during slow landscaping seasons. How much can you save when revenue is low or if the economy crashes?

3. Assess your resources

Take stock of your current financial resources. What are your current income sources, business assets, and expenses?

Do you have social security benefits? If you’re an employee, do your employers offer a retirement plan?

Once you’ve identified current resources, think about how to grow and diversify your investments even in retirement. Assessing your current resources helps you identify the gap between where you are and where you need to be.

4. Select a retirement account

For business owners, choose a retirement plan that reflects your goals. Here are some options to consider:

SEP IRA: This is simple to set up and an excellent option for businesses whose profits fluctuate.

Solo 401(k): Ideal for higher contributions if you’re a solopreneur.

Traditional or Roth IRA: Great for tax advantages and personal savings.

5. Get to work

Now that you have a clear insight into your retirement plans, set up automatic transfers into your accounts. It can be 10% of your gross income or at least $50. The bottom line is to just start—perhaps with something you’re comfortable with, and then build from there.

How much should landscapers save for retirement?

According to the U.S. Department of Labor, workers will need 70–90% of their pre-retirement income to maintain their standard of living after they stop working.

While there’s no generally accepted percentage that landscapers should save, Dave Ramsey, a popular financial expert, recommends 15% of your gross income. This percentage, Ramsey says, helps you build a solid nest egg and leaves room for other financial goals.

Now, the reason there’s no recommended percentage for landscapers is that there are different factors involved:

Desired retirement age: Planning to retire early means you need to save more than you would for a normal retirement. So if you plan to retire at, say, 60 instead of 67, you’ll have more years to fund and fewer years to save for it.

Retirement lifestyle: Do you plan to travel or live simply? Would you downsize or maintain your current lifestyle? A comfortable lifestyle means you will need to save more income from the landscaping business.

Inflation: Prices will change over time. You need to factor that into the retirement savings to maintain your purchasing power.

Health status and longevity: Years of physical labor can lead to earlier health issues, limiting a landscaper's ability to remain active.

What are the best retirement savings options for landscapers?

Here are the top savings options you may want to consider:

Solo 401(k)s with Roth Option: This savings plan is flexible, supports high contribution limits, and allows for Roth contributions. With this option, you can pay your taxes now and avoid them post-retirement.

In addition, you can make contributions as an employer and employee. This helps you make good contributions when the business is doing well and comfortably reduce them in leaner seasons.

Overall, it’s ideal for business owners with part-time workers or subcontractors, as it allows maximum flexibility.

SEP IRA: This offers similar flexibility to 401(k)s but is low-maintenance, without the Roth and tax-free options. Here, landscapers can contribute up to 25% of net earnings from self-employment. It provides allowances for future employees, but workers must receive the same contributions as the employer, which increases costs.

Backdoor Roth IRA: Here’s another retirement savings plan that supports tax-free distributions during your retirement. It places no limit on how much income you can contribute, recognizing that your income may grow over time.

When should landscapers start planning for retirement?

The best time to start retirement planning is now, regardless of your age or experience level. This ensures you have more control, more options, and greater peace of mind about your future.

Jonathan Christian of Florida Turf recommends starting in your 20s or 30s. He explains how profitable it is to start early with a retirement calculator. Contribute $300 monthly to your retirement funds for 40 years at an annual rate of return of 10%, and the future value could reach $1.6 million.

The point is that the earlier you start, the more time your funds have to grow through compound interest. Plus, it gives you time to adapt if things don’t go as planned, whether because of health issues or lean landscaping seasons.

But if you start later—e.g., in your 40s or 50s—remember, it’s never too late. Your best option is to start now. You just need to budget more intentionally and take advantage of catch-up contributions, and you can still retire comfortably.

Is it ever too late for landscapers to start saving for retirement?

No, it’s never too late to start saving for retirement. While it can definitely feel frustrating, you can still build a solid retirement plan using the following strategies:

Avoid lifestyle inflation: Try to live way below your earnings and divert extra funds to retirement savings.

Double down on investments: Beyond a retirement savings account, consider increasing your investment allocation and diversifying.

Allocate pay increases to retirement: Divert raises, bonuses, or tax refunds into your retirement savings.

Maximize catch-up contributions: You can make additional catch-up contributions to retirement savings accounts beyond the standard limits. For instance, while the annual limit for 401(k)s, 403(b)s, and 457 plans is about $23,500, catch-up contributions let you add $7,500 extra.

Start immediately: Lastly, make plans to get started now. Set up automations to ensure your retirement funds are transferred seamlessly every month.

How can landscapers sell their business to fund retirement?

Selling your landscaping business can be everything you need to achieve your retirement goals. Here’s how you can do that:

Prepare the business for sale: First, improve its value and make it more attractive to potential buyers. Do that by expanding operations, streamlining business financial records, and delegating tasks so the business runs without you.

Evaluate the business: Review your client contracts, service diversity, business size, financial health, and market position. This will help you assess your current situation and identify gaps you need to fill.

Decide when to sell: The ideal time is when your profits are surging upward. But you also want to consider when you want to retire and the market conditions, so the sale is profitable.

Define your ideal buyer: Are you considering a third-party or an in-house purchase? If it’s in-house, is your successor ready for the role? For external buyers, how would you define them, and what conditions must they meet before you sell to them? This could be their net worth or decision to retain existing staff.

Market the business: Hire a business broker to market the business and handle negotiations until a deal is reached.

How can landscapers maximize retirement income?

You’ve decided to start saving for retirement, but that alone might not be enough to help you achieve your goals. Here’s how you can maximize your retirement income and make it last longer:

Diversification: Don’t put all your eggs in one basket. While retirement accounts like the 401(k) are good, you can invest in real estate, purchase stocks or bonds, or pay for Social Security. You could also increase your income by becoming a consultant or a landscape content creator like Jonathan Christian of Florida Turf.

Control your expenses: Try to curb spending both now and in retirement to increase your savings. Consider relocating to a more affordable area, cancelling unnecessary subscriptions, or downsizing your home or vehicle.

Plan for healthcare: Health costs are one of the biggest expenses you’ll have to deal with. You may want to save into a Health Savings Account while still working, so you’re prepared.

Work with a financial expert: Hire someone who understands business and finance to help you navigate retirement income. They can help with a withdrawal strategy so you know which account to take from or how to rebalance investments.

Keep the business working for you: This option offers different choices. Rent out functioning equipment and vehicles you rarely use. Hire a competent manager to run the business so you can earn passively. Just ensure it’s someone tech-savvy who can use digital tools like Aspire to streamline and manage operations.

How Aspire helps landscaping business owners prepare for retirement

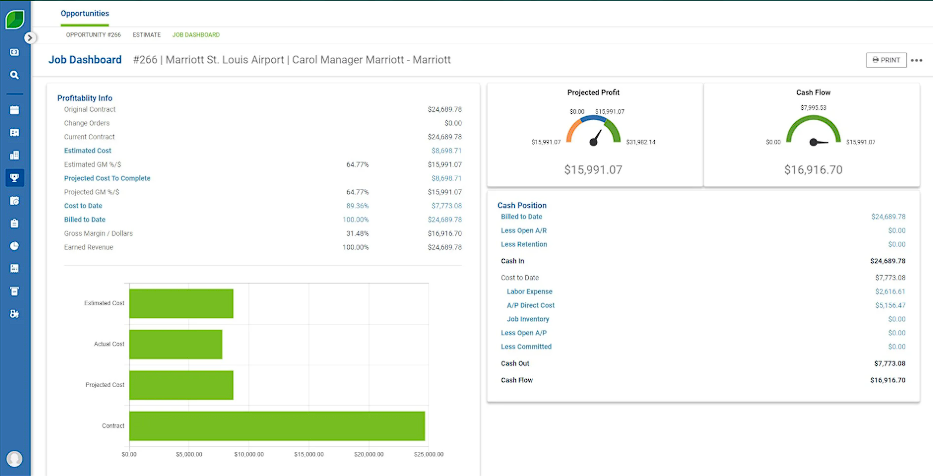

Aspire is a field service management app that allows landscaping businesses to streamline operations, enhance profitability, and drive growth.

With features such as scheduling, estimating, CRM, job costing, time tracking, and reporting, you can have a detailed overview of how your landscaping business runs. It lets you see whether you’re running at a profit or a loss.

This bird’s-eye view enables you to identify which landscaping service can contribute to your retirement savings more consistently. Plus, you can identify growth opportunities to increase the business’s value.

With Aspire, it’s easy to manage every aspect of the company—from crew performance to client contracts, incident reports, finances, estimates, invoicing, payment, and more. Simply put, it keeps the business organized, efficient, and attractive to potential buyers when it’s time to exit.

Want to see how it works in real time?

Schedule a demo with Aspire today.